5th May 2016 With $2.9 billion in debt covenants and inter-company loans due in 2016 Vedanta is turning to increasingly controversial and irregular methods to bleed cash from its few profitable subsidiaries. Having already asset stripped the Zambian Konkola Copper Mines, being prevented by an employees union from getting access to Hindustan Zinc Ltd’s $4.6 billion cash reserves, and by shareholder action from getting hold of Cairn India’s cash, Vedanta are now paying themselves ridiculous 1200% dividends in a desperate attempt to grab the cash and keep the lenders happy.

5th May 2016 With $2.9 billion in debt covenants and inter-company loans due in 2016 Vedanta is turning to increasingly controversial and irregular methods to bleed cash from its few profitable subsidiaries. Having already asset stripped the Zambian Konkola Copper Mines, being prevented by an employees union from getting access to Hindustan Zinc Ltd’s $4.6 billion cash reserves, and by shareholder action from getting hold of Cairn India’s cash, Vedanta are now paying themselves ridiculous 1200% dividends in a desperate attempt to grab the cash and keep the lenders happy.

Vedanta Ltd was India’s second most indebted company in June 2015 with $12 billion of debt. Parent company Vedanta Resources has a net debt of $8.6 billion (Jan 2016) and inter company loans of $1.8 billion. The Wall Street Journal this week reported that Vedanta Resources’ debt is officially 5.7 times Ebitda ‘but in reality it is more like seven times Ebitda when only considering the parent’s actual claims on cash at its subsidiaries’ and called this a ‘dire picture’. Much of this debt is due to losses incurred at Vedanta Resources’ Indian subsidiaries (now incorporated into the Indian wing of the company Vedanta Ltd) as a result of Vedanta’s illegal activities and local protests against them. The mining ban in Goa in which Vedanta subsidiary Sesa Goa was indicted for illegal mining and mis-declaring export figures stopped all production for almost two years, and the successful movement against the Niyamgiri bauxite mine on indigenous land in Odisha is estimated to have cost the company up to $10 billion in lost investment.

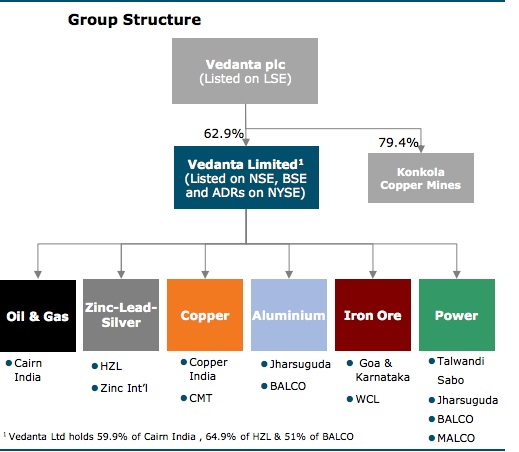

Vedanta’s current corporate structure. Perhaps in an attempt to hide this loss making entity the Niyamgiri/Lanjigarh project – previously Vedanta Aluminium Limited – is not listed as part of the aluminium business in Vedanta’s new corporate structure.

To keep the company afloat Vedanta has used routinely used irregular and illegal practices to transfer cash or liquidate assets from profitable subsidiaries in order to meet debt repayments. In July 2014 a $1.25 billion loan had been transferred from Vedanta’s cash rich oil and gas subsidiary Cairn India to Sesa-Sterlite (now Vedanta Ltd) without seeking minority shareholder approval. The loan was used to pay $800 million of principal and $450 million of interest on another inter-company loan, possibly the very loan that was made to the parent company Vedanta Resources by Sesa Sterlite to buy majority shares in Cairn India when it was acquired in 2011. Minority shareholder Rajotavo Dasgupta subsequently sued Cairn India for violation of rules on arms length trading and related party transactions, fearing that the loan would be written off if Vedanta Ltd (previously Sesa Sterlite) merged with Cairn India as planned. Cairn India is now seeking a rollover of the loan at the end of the two year loan period, raising further fears that it will not be paid back.

In Zambia, government audits of Vedanta subsidiary Konkola Copper Mines in July 2014 revealed that Vedanta have essentially asset stripped the mines, selling off trucks and equipment, failing to maintain collapsed shafts and using up cash reserves. KCM had also failed to pay contractors or invest any CAPEX in the subsidiary, and paid the parent company exorbitant annual management fees. The company were also exposed for transfer pricing – selling their own copper, gold and silver underpriced to their subsidiary Fujairah Gold, run by Vedanta boss Anil Agarwal’s son Agnivesh in Dubai, evading vast quantities of tax in Zambia and pocketing undeclared profits of $500 million per year.

In December 2013 Vedanta slipped from the FTSE 100, falling out of favour with European banks, and began turning to Indian state banks for loans, shifting their debt burden onto the Indian taxpayer and contributing to the Indian corporate debt crisis, documented in Credit Suisse’s ‘House of Debt’ reports. In February 2016 the combined debt of the 17 most highly leveraged Indian companies was more than 8 times Ebitda, compared with 5.5 times a year earlier.

In January 2016 Vedanta bought back $500 million in convertible bonds which were due in July 2016. Bank of America Merrill Lynch rated Vedanta as the second riskiest corporate junk bond on the market and Trader Jens Zimmerman told Bloomberg; “Bond prices at these levels show us that there is no trust for the company, so refinancing could be a problem in the future.”

Next Vedanta focused on the cash reserves of its wealthier subsidiaries to pay off upcoming debt covenants such as the $2.9 billion due in 2016, attempting a buyout of the remaining 29.5% Indian Government stake in Hindustan Zinc Ltd (HZL), which has $4.6 billion in cash reserves, and a merger between Vedanta Ltd and Cairn India to gain access to Cairn’s $2.85 billion reserves. However, the Cairn merger is currently delayed due to minority shareholder action, and the HZL buyout has been quashed by the Supreme Court of India as unconstitutional, following a case filed by an employees union.

With commodity prices at a very low ebb and major debt covenants fast approaching Vedanta is now making major dividend payments from profitable subsidiary HZL, one of the only remaining ways of transferring some of the cash to the parent company and majority shareholder. On March 30th 2016 HZL (like Fujairah Gold chaired by Anil’s son Agnivesh Agarwal) declared a ‘special golden jubilee dividend’ for 2015-16 at a rate of 1200%, effectively paying parent company Vedanta Ltd $1.2 billion. Cairn India may also make dividend payments in the coming weeks.

Despite this on 6th April Chairman and founder Anil Agarwal went on a press offensive to create confidence in the company stating that, “We have enough resources to service our debt. In fact, we keep reducing our debt every year” by using funds from free cash generation, and even claiming that “We will spend over $2 billion in the next two years, mostly in oil and gas, if some government clearances that we expect come through.” There is a formula for understanding Vedanta’s financial position – the more gushingly optimistic statements Agarwal and CEO Albanese make to in the media, the worse trouble they are actually in.http://www.foilvedanta.org/articles/vedantas-toxic-debt-tricks/

Leave a Reply